Where did reverse mortgages come from? Why is the government so heavily involved with offering them via the Home Equity Conversion Mortgage (HECM)? How has the industry changed over the years, and where might it be heading next? We’ve compiled our research in an attempt to answer these questions.

Stick with us, and we’ll do our best to explain to you:

- The evolution of reverse mortgages from conception to present day

- Changes in the HECM program over time and the reasons why

- Changes in borrower characteristics over time and the reasons why

- Public perception of the product and how it came to be

Origins of Reverse Mortgages

The United States is a homeowner society, and owning your own home is a large part of the American dream. Since at least the 1930s, the US government has actively encouraged homeownership both directly through institutions like Fannie Mae and the Federal Housing Administration (FHA), and this support only increased post-World War II. Homeownership rates in the country are among the highest in the world.

One consequence of high homeownership rates is that many Americans end up with large amounts of home equity, which is the value of the home minus the balance of the mortgage. Though this equity represents real wealth, the only obvious way to access it is to sell the home. In 1961, Deering Savings & Loan in Portland, Maine originated the first reverse mortgage, a specialized product designed to help older homeowners access their home equity without needing to sell. Other private lenders offered similar products throughout the 1970s, but adoption rates never took off.

The American Government Gets Involved

By 1982, the Special Committee on Aging met to discuss how the government could help older homeowners access their home equity. Here are a few interesting points that the committee raised, the first and last of which are attributed to Senator John Heinz, the second attributed to Ken Scholen, an activist.

On the needs of the American people:

The total value of the equity held by older Americans is over $600 billion. Obviously, millions of older Americans could greatly benefit from the ability to draw on home equity to meet monthly income needs, to finance home repair and maintenance, or to pay major medical expenses.

On the failure of the private mortgage lenders to serve this population:

On a simple term product, you could insure the cash flows for the borrower and

the encumbered equity for the lender. On a long-term reverse mortgage, by contrast, you are pooling a number of different risks-mortality, mobility, casualty, appreciation- all in one instrument. That is an uncommon combination of risks, and no one knows how it will play out over a period of time.

More on the failure of the private market:

What you are saying, in effect, is that the risk associated with a single individual arrangement may be so difficult to figure out that, unless you find a way of pooling the risks into some kind of insurance pool where there is more of an actuarial certainty, that it is difficult or somewhat unlikely that a sufficient number of lenders or investors will come forward.

Throughout American history, the government has stepped in to provide certain goods and services like defense and public roads and highways. Generally, these are known in economics as public goods, and they cannot be provided privately because it would be difficult for a private company to receive payment from those using the goods. The idea behind reverse mortgages is somewhat similar, and it has even more in common with the public risk pooling of programs like Medicare.

For a very thorough argument for the need for government action, we recommend this paper by the Mortgage Professor, Jack Guttentag. In it, he argues that the program would provide enormous benefits to older homeowners, many of whom are impoverished, while costing very little to the American taxpayer.

The Home Equity Conversion Mortgage

In 1987, these discussions turned into action with the Housing and Community Development Act. This act launched the Home Equity Conversion Mortgage (HECM), and in 1988 the Department of Housing and Urban Development (HUD) gained the ability to insure these loans through the Federal Housing Administration (FHA).

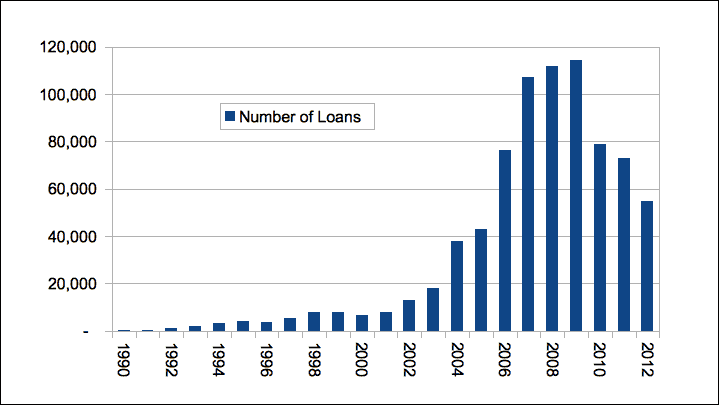

The program began as a pilot with low caps on the number of originations allowed each year. Reverse mortgages were also available only as adjustable rate products, and by 1996 the market was dominated by loans that adjusted monthly rather than annually. In 1998, the HECM program became permanent, and the cap was raised to 150,000 loans per year.

The market for reverse mortgages rose slowly, then it began to rise rapidly in the early to mid 2000s as the American housing market boomed. From 2002 to 2003, originations jumped from 109,949 to 131,286, an increase of nearly 20%. Here is a chart of HECM originations from 1990 to 2012; the data are from HUD.

The Rise of the Fixed-Rate HECM

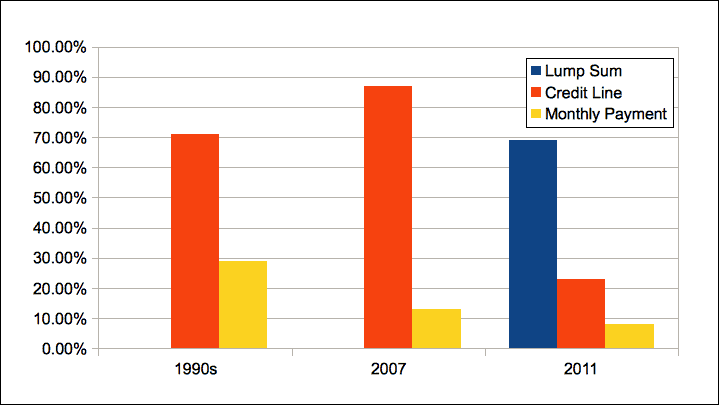

When adjustable rate reverse mortgages were the only option available, borrowers could only receive the proceeds in the form of a credit line or monthly payment with a small upfront lump sum payment. Although there are cases where it makes more sense to receive a lump sum up-front payment – to pay off an existing mortgage, for example – in general a borrower is better off picking on of these options.

Everything changed in 2008. First, the FHA changed the rules on how reverse mortgages could be structured, allowing for a fixed rate product where the borrower took a lump sum at closing rather than receiving money over time. Ginnie Mae, a government corporation within HUD, began securitizing fixed rate reverse mortgages, greatly increasing the incentive for lenders to focus on these products.

Virtually overnight, the market shifted from adjustable rate loans where the proceeds were withdrawn over time into fixed rate mortgages where the borrower took a lump sum payment. Here’s a graph showing how borrowers chose to receive proceeds. The data come from the Federal Reserve.

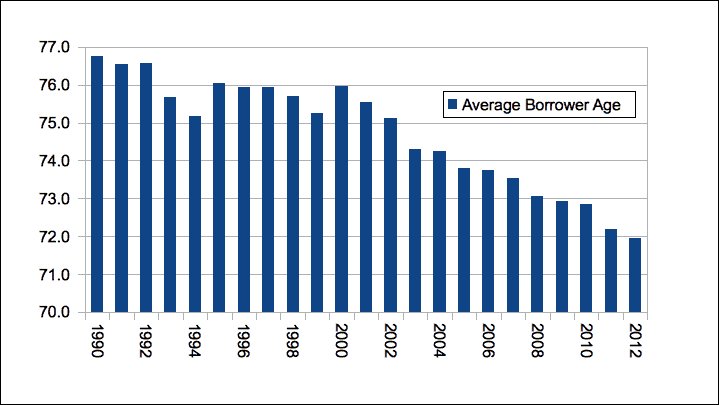

This chart actually understates the problem, however, as it does not tell us how much money the borrowers were taking at closing. In 1990, near the beginning of the HECM program, borrowers were on average withdrawing around 36% of the principal limit. By 2008, the year the fixed rate product was introduced, this number had soared to 80%. The average of a borrower also began to skew younger. Homeowners were using up more home equity early on, leaving little to meet needs such as medical expenses in later years.

The Consequences

The market shift would have dramatic consequences for both borrowers and the FHA. By February of 2012, 10% of reverse mortgage borrowers faced a tax and insurance (T&I) default, which occurs when the senior fails to keep current on property taxes and homeowner’s insurance, both of which are required in the terms of a HECM loan. As this analysis indicates, the problem was overwhelmingly caused by the new fixed rate loans.

Although it does not appear that these seniors lost their homes to foreclosure – the FHA has been very resistant to foreclosing on borrowers, and within reason – they are at risk of losing their homes. Additionally, a borrower who cannot make T&I payments may not have the money to pay for everyday living expenses or emergency medical care. These borrowers have already used up a valuable asset, their home equity, and it is very possible that for many nothing else remains.

For the FHA, this means increasing losses to its insurance fund. The HECM program was largely promoted as a low cost solution to a big social problem, but fixed rate HECMs appear to have been very expensive for all involved.

The issue culminated in an excellent report by the Consumer Finance Protection Bureau in 2012. The report is well worth a read, as it covers almost everything one could want to know about reverse mortgages and the HECM program. The CFPB drew five major conclusions:

1. Reverse mortgages are complex products for consumers to understand.

2. Reverse mortgage borrowers are using the loans in different ways than in the past, which increases risks to consumers.

3. Product features, market dynamics, and industry practices also create risks to consumers.

4. Counseling, while designed to help consumers understand the risks associated with reverse mortgages, needs improvement in order to be able to meet these challenges.

5. Some risks to consumers appear to have been adequately addressed by regulation, but remain a matter for supervision and enforcement, while other risks still require regulatory attention.

Unquestionably, the first and second point were driven largely by the rise of fixed rate HECMs.

The FHA Adjusts

In 2013 and 2014, the FHA announced major changes to the HECM program which are widely believed to be positive for almost everyone. In April 2013, the fixed rate product was discontinued once and for all. The effect was almost immediate – by the summer, industry experts were reporting that originations were over 90% adjustable rate.

Later in the year, the FHA limited the up front lump sum payment to 60% of the principal limit in the first year. As we saw earlier, median withdraws had reached 80%+, making this a big change. Principal limits were also reduced across the board, further reducing lump sum initial payments. Michael Kitces provides an excellent rundown of these changes here.

In 2015, the FHA began requiring borrowers to undergo a financial assessment before obtaining a reverse mortgage. This assessment determines whether the borrower will be able to make monthly T&I payments going forward.

The Road Ahead

In our opinion, the HECM program has been changed for the better, and the timing could not be better – with millions of Americans approaching retirement, there is going to be a large need for reverse mortgages in the very near future.

The FHA also eliminated the HECM Saver program, a special reverse mortgage with a very small initial MIP payment. The authors see an excellent opportunity for proprietary products with lower principal limits but also lower fees that would be ideally suited for borrowers who want a cheaper, more short-term reverse mortgage.