The Truth About Early Retirement

Introduction

Is early retirement something that appeals to you? Many of us dream about retiring early, and it’s easy to understand why – not having to wake up early, get dressed, and go spend the majority of your day working for someone; the freedom to do what you want, when you want. Imagine how much more enjoyable life would be if you didn’t have to work but still had enough money to live comfortably.

If early retirement is one of your dreams, and something you truly want to experience, then the good news is that this goal is well within your reach. The average retirement age in the United States is around 63 years old, and nearly 20% of Americans are able to retire even earlier.

You’ll need to be both disciplined and creative, and you’ll benefit greatly if you start preparing as soon as possible. By planning and saving early and making the commitment to stick to these plans, then you have a very good chance of retiring early. You don’t even need to have millions of dollars in the bank to do it.

That said, is early retirement a good idea? Do the pros outweigh the cons? Just because you can retire early doesn’t necessarily mean that you should. By leaving the work force early, you’ll be foregoing your salary and the ability to grow your nest egg. You may also find that you simply don’t enjoy your retirement quite as much as you thought you would.

We’re here to help you understand what it takes to leave behind your 9 to 5 job a little earlier than most, along with an honest look at the pros and cons of early retirement. We cover:

- How much you need to save before you can retire

- Steps you can take to accumulate the necessary savings

- A few downsides of early retirement that you may not have considered

- The benefits of starting your path to early retirement right now

By the end, we hope to give you a better idea of what it takes to retire early and the tools to decide whether this is right for you. Let’s get started.

How Big of a Nest Egg Do You Need?

If you’ve just started thinking about early retirement, you may be confused about where to begin. With that in mind, here’s a logical first question to ask – how much do you need to save before you can retire?

The next steps are to figure how much money you’ll need each year and determine how much of this retirement income will need to come from your savings. Will you have alternate streams of income, such as a pension or a side job, or will you need to take 100% of this cash from your nest egg? For most people, the answer is somewhere in between, but we’ll assume you need to replace 100%.

Step 1: Estimate Your Disposable Income

How much money will you need each year of your retirement to live comfortably? A good estimate is that you’ll need the same disposable income that you currently have coming in annually. You can arrive at this number by subtracting your taxes from your current income (salary plus any other money you’re bringing in), though a more accurate estimate might involve subtracting:

- Mortgage payments

- Retirement savings contributions

- Work expenses, like transportation to and from your job

This is a good starting point in trying to determine what you’ll need to replace once you retire early.

Step 2: The Quick & Dirty Four Percent Rule

In the 1990s, a financial planner developed a popular rule of thumb known as the four percent rule. Although it’s woefully outdated – a 2013 study published in the Journal of Financial Planning found that following this rule is simply too risky in today’s low interest rate environment – it’s a reasonable jumping off point for our purposes.

The rule states that if you withdraw 4% or less of your retirement savings each year, then you have a large enough nest egg to fund your retirement. The calculation is quick and easy, so take the disposable income that you estimated and go ahead and run the numbers yourself. Just remember to take the result with an appropriate grain of salt.

Here’s are two examples to demonstrate:

$20,000

Annual Withdrawals- $20,000 / 4% = $500,000

$40,000

Annual Withdrawals- $40,000 / 4% = $1,000,000

Building Your Early Retirement Nest Egg

Now that you’ve got a rough estimate of how much you’ll need to retire early, it’s only natural that you’re wondering how to reach this savings goal. The good news is that the answer isn’t complicated; the bad news is that there’s no shortcut or magic bullet.

One half of the equation is to maximize your earnings, whether it’s your salary or the income you earn from your savings & investments. The other half of the equation, and equally important from our perspective, is to reduce your expenses and increase your savings while maintaining a comfortable lifestyle.

Maximize Your Earning Potential

It should go without saying that earning more money will enable you to save more money, which will in turn help you to retire earlier. There are many ways to earn money, and you can find countless strategies for starting a “side hustle” across the Internet. We’ll focus on attacking this goal from the angle that provides the best bang for your buck – increasing your earnings at the job you already have (or hope to have someday).

Invest in Your Education

One great way to earn more money over the long haul is by investing in your education. Although education will typically cost you money, as long as you do your research beforehand you can make sure that it’s money well spent. Think of your education as an investment instead of an expense.

College: According to a recent study by the Economic Policy Institute, college graduates earn 56% more than high school graduates.

Other options: Graduate school, relevant industry certifications, webinars & other online options.

Negotiate a Higher Salary / Ask for a Raise

Are you earning what you’re really worth? Take the initiatve and find out what other people with similar job titles are earning. It’s fast and easy to do on websites like Indeed.com and Glassdoor.com. Armed with this knowledge, don’t just wait around for your company to give you a raise – go and ask for one, with a specific number in hand.

Get a Promotion

Keep your eye out for openings within your company and pounce on a relevant one when it appears. Be ready to make the case for why you’re the perfect fit for this new job.

Put Your Money to Work for You

Saving money is great. You should absolutely have an emergency savings fund that you can access should you need money quickly. However, a savings account is not where you should be putting your money when you are building a retirement fund. Where should you put your money then? One of the best options is a 401(k).

What is a 401(k)? In simplest terms, a 401(k) is an employer-sponsored retirement fund that offers a lot of advantages to anyone who is serious about saving for retirement.

What advantages does a 401(k) offer? The biggest advantage of a 401(k) is that most companies that offer them match employee contributions to a certain extent. So, if you have 5% of your check deposited into your 401(k) account, and your employer matches it, then you are saving 10% of your paycheck even though you are only paying 5% of that yourself. In other words, it’s free money. Free money is always a good thing! Another advantage of a traditional 401(k) is that the money you contribute toward your retirement is taken out pre-tax. That means since you don’t pay taxes on it, you can actually lower your taxable income, and your tax bracket, by increasing your 401(k) contributions. The catch to all of this is that when you reach retirement age and begin to withdraw money from your 401(k), then it is taxed.

Now, if you are looking at early retirement then there may be a better option for you than a traditional 401k. That option is a Roth 401(k). A Roth 401(k) is identical to a traditional 401k, except you deposit money into your retirement savings after your paycheck is taxed. This eliminates many of the tax benefits of a 401(k), so why should you consider a Roth 401k instead of a traditional one? You should consider it because you are not taxed on it when you start to withdraw the funds. Since you have already paid your taxes on it when you earned it, the money is now all yours. This is hugely beneficial for retirees since you can generally afford to pay more in taxes when you are actually working, as opposed to when you are retired. A Roth 401(k) also has the benefit of allowing you to withdraw contributions both tax and penalty free at any time, although you do have to wait until you are 59 1/2 to withdraw any earnings.

Of course, you can also utilize both a traditional 401(k) and a Roth 401(k)!

Reduce Your Expenses

“It’s not what you earn, it’s what you keep.” We’ve all heard the saying, and it’s true – by reducing your expenses and saving that money instead, you can greatly accelerate your path to early retirement.

True, you’ll need to have the self-restraint to avoid spending money on things that you really don’t need. Will it be tough? Sometimes, but there are simple changes you can make to minimize the pain while saving a nice chunk of change. And remember, every penny you spend is a penny that is gone forever.

With that in mind, we’ve put together some suggestions for making minimizing your expenses a priority without living like a pauper.

Pay Off That Mortgage

One thing you shouldn’t be afraid to spend more money on is paying down your mortgage. Your home is more than a place to live, it’s a major investment. When you retire you want to retire without owing any money on your mortgage. This gives you a place to live without having to worry about paying for it once you quit working. One great way to pay your home off faster is to make payments bi-weekly instead of monthly. You don’t have to pay more, you just split your normal monthly payment into bi-weekly payments. Doing this can help you to pay your home off several years early, and save you thousands of dollars in interest.

How Much House Do You Really Need?

There’s a popular question among home buyers – how much house can I afford? If you want to retire early, a more appropriate question to ask is how much house do I need? According to Tanja Hester, author of Work Optional: Retire Early the Non-Penny-Pinching Way, reducing your housing costs is one of the quickest, least painful, and most impactful ways to save for an early retirement.

For example, imagine that you’re a single person living in a two bedroom apartment and paying the national average of $1,200 per month. If you instead choose to live in a $950 one bedroom apartment, you will save an additional $250 each month, or $3000 per year. You’ll have less space, but you probably don’t need all the space you currently have and may not even miss what you’re giving up!

Spend Less on Transportation

After housing, the next major expense that most people have is transportation. In 2018, the average monthly car payment was over $500. Add in another $100 for insurance, and you’re looking at over $7000 per year on your car before even considering gas!

So, how can you reduce or even eliminate this expense with the minimum amount of pain? Here are a few ideas from Work Optional:

- Consider living somewhere walkable where you won’t need a car

- Get a used car instead of something new

- Keep your car for as long as possible

The Cons of Early Retirement

Are there any disadvantages to retiring early? Generally speaking, when it is properly planned for, early retirement is a good thing. However, there are a few potential drawbacks to consider before deciding if this is the right path for you.

Did You Really Save Enough?

Choosing to leave the workforce early while lacking sufficient financial resources can prove to be a mistake. If you are planning on retiring early, make sure that your finances are in order. This means going beyond the simple rules of thumb that we talked about earlier and really analyzing your situation and how much you will need.

What About Health Insurance?

It’s easy to overlook healthcare when contemplating early retirement. Make sure you have a plan for replacing any insurance that you currently get through your job – Medicare eligibility doesn’t start until age 65, and if you’re considering early retirement that could be a long way away.

Consider the Social Benefits

You should also weigh in the level of enjoyment and interest that you get from working. Working a job provides physical and mental stimulation, and some people begin to decline after retiring. Make sure you have a plan in mind to replace these underrated benefits of holding down a job!

Start Planning Early

If you want to retire early, your best bet is to realize this from a young age and begin to plan and strategize appropriately. No matter how old you are, you will best served if you start planning and taking action as soon as you can.

Saving money from the moment you start working (or as close to it as possible) will make a huge difference. It doesn’t matter if it’s a relatively small amount. As long as you are saving something, and not touching that money, then you are on the right track.

The Power of Compound Interest

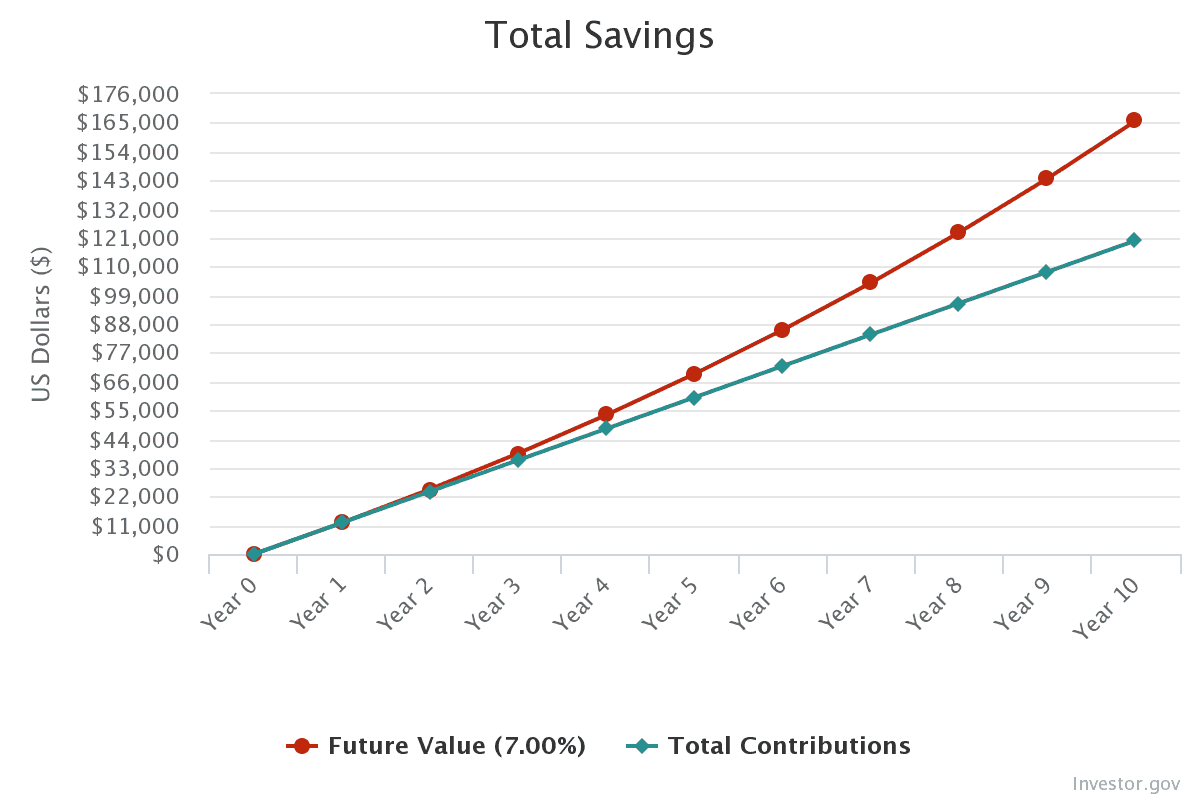

For example, let’s imagine that you’ve taken some of our advice above and are now saving $1000 a month more than you were before.

Now imagine that you’re able to earn a 7% annual return on these savings and assume you aren’t paying taxes on what you earn because you’ve chosen an appropriate 401(k). After 10 years, you’ll have deposited $120,000 and earned over $45,000 in interest:

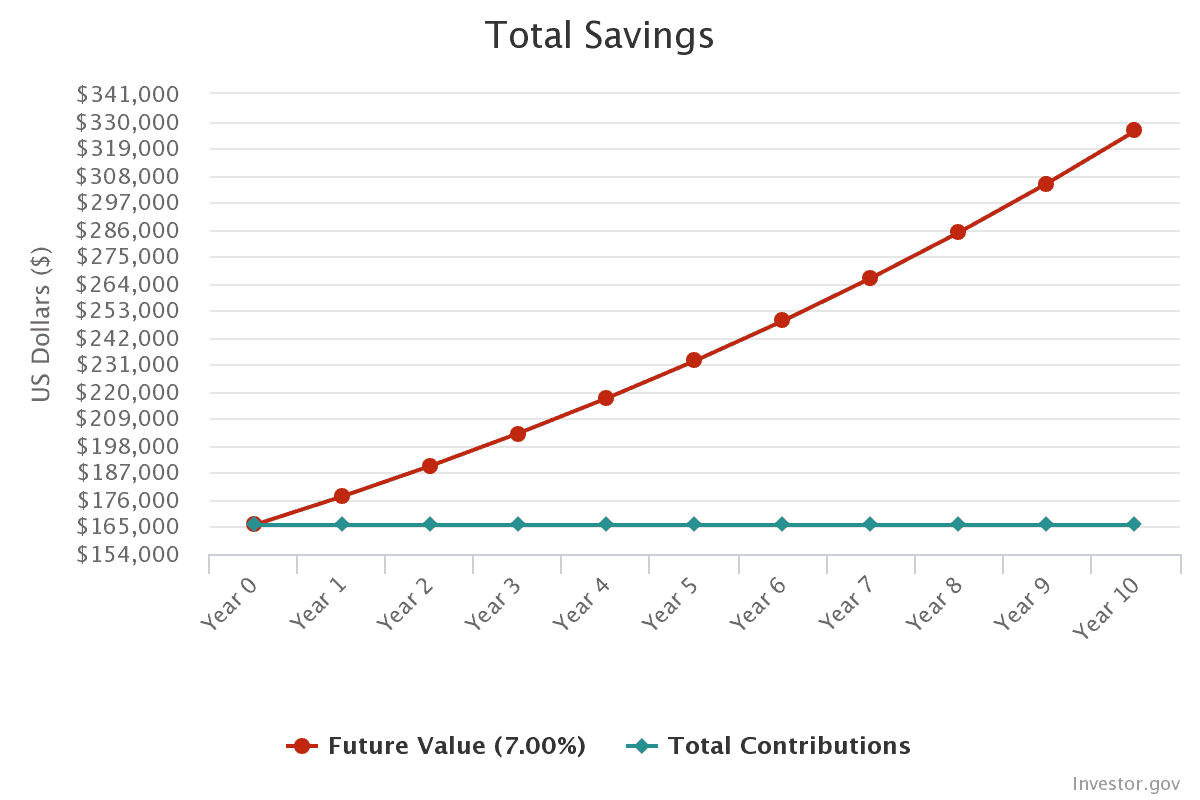

If you keep this money in your retirement account for another ten years, the value of your nest egg will have grown to over $326,000:

That’s the power of compound interest, and it’s the reason why you should start saving immediately if you want to retire early.

Resources

Is early retirement possible?, Marketwatch

What You Need to Know About Early Retirement, Reader’s Digest Canada

The 4 Percent Rule Is Not Safe in a Low-Yield World, Journal of Financial Planning

Work Optional: Retire Early the Non-Penny-Pinching Way, Tanja Hester via Amazon.com

Why you might want both a traditional 401(k) and a Roth, CNN Money

Compound Interest Calculator, Investor.gov – U.S. Securites and Exchange Commission