Why care about reverse mortgages in the first place? Based on data from the United States Census Bureau, only 2-3% of eligible Americans have a reverse mortgage, which suggest this is merely a niche financial product that appeals to a minority of seniors. We care because there are many large, important forces at play that seem destined to turn reverse mortgages into an essential financial tool for far more seniors in the future. In this article, we’ll cover demographic trends, rising health care costs, and the looming potential for a retirement crisis. By the end, we think you’ll understand how important the reverse mortgage could be over the coming decades.

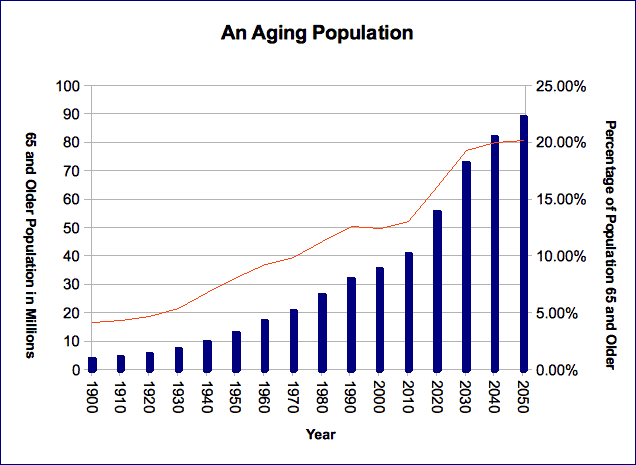

An Aging Population

You’ve likely heard that the American population is growing older. It’s true, and in fact it understates what is really happening. When the 2010 census was taken, there were a little over 40 million Americans who were 65 and older, making up a little over 10% of the population. Both numbers have been rising steadily for years. The Census Bureau also makes projections into the future; we put together this chart based on these projections. The data from 1900 to 2010 are recorded statistics, the data from 2020 to 2050 are projections.

The authors were amazed when we first put together this chart. In just three decades, the number of seniors in the United States will more than double. The population will be composed of more older Americans than at any point in the country’s history.

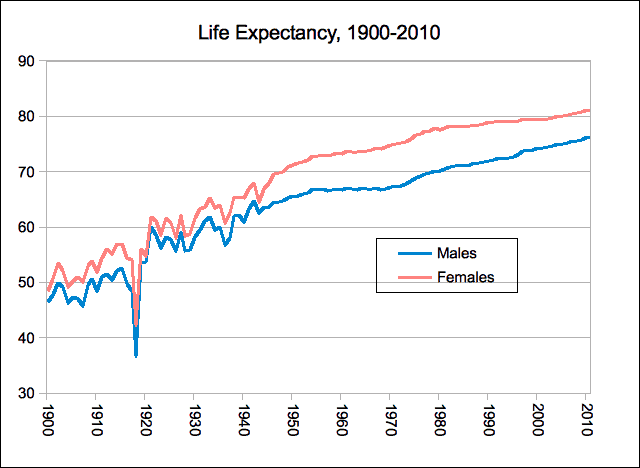

Increasing Lifespans

We’ve established that America is getting older, but what does this mean? One big reason for this demographic shift is that Americans are living longer. This chart, compiled from data located here and here, shows life expectancy at birth from 1900 to 2010.

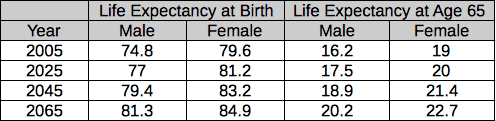

According to this report, the trend will continue far into the future. Here’s a table showing life expectancy projections, both at birth and at age 65:

Americans are living longer, and don’t get us wrong – this is a great thing. However, these trends also tell us that the seniors of today and the not-too-distant future will have much longer retirements than previous generations. By 2065, your average 65 year old American female can expect to live an extra 4 years. We all want to live in a society where she will be able to live those years at a comfortable standard of living.

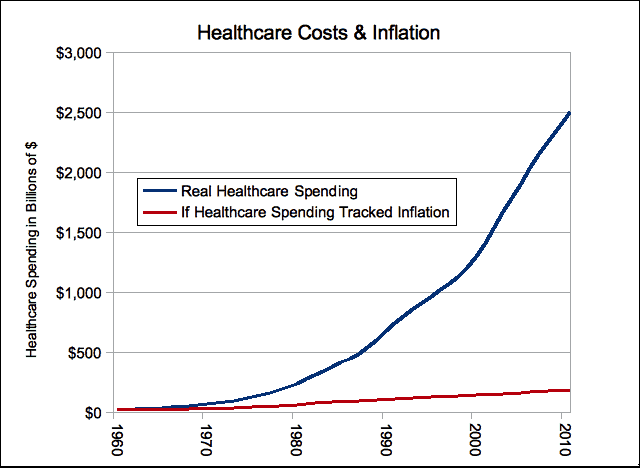

Rising Healthcare Costs

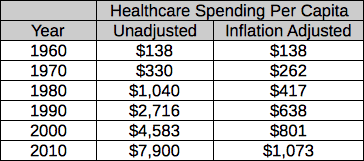

Access to good healthcare is an important factor in maintaining a senior’s standard of living. Unfortunately, these costs are rising dramatically and show no signs of slowing down. We put together this chart to show how healthcare costs have risen over time. The data, taken from here, show total healthcare expenditures in the United States from 1960 until 2010. We also took the initial figure in 1960, $24.763 billion, and figured out how much it would’ve increased each year just due to inflation, using this data.

This is a crude way to explain rising healthcare costs, so let’s find a better one. One is to look at how much each American is spending every year on healthcare over time. In 2010, multiple outlets reported that Americans spent between $8,200 and $8,400 each year on healthcare. We couldn’t find historical data, so we put together the table below using historical healthcare spending, census data, and accounting for inflation. You’ll notice our 2010 figure is a little below $8,000, which means that we’ve chosen to be slightly less precise for the sake of showing historical trends. Here is our table of historical per capita healthcare spending:

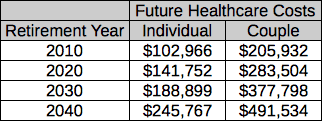

That is a very large increase. We know that seniors spend more money on healthcare than younger Americans. Here is a table based on data from the Center for Retirement Research at Boston College showing how much an individual or couple retiring in a given year will need to have saved up to cover future healthcare costs.

As of 2010, a couple would need to have over $200,000 on hand just to cover their expected healthcare costs into the future! These are out of pocket expenses, so factors such as Medicare have already been factored into the calculation.

The Rising Costs of Long-Term Care

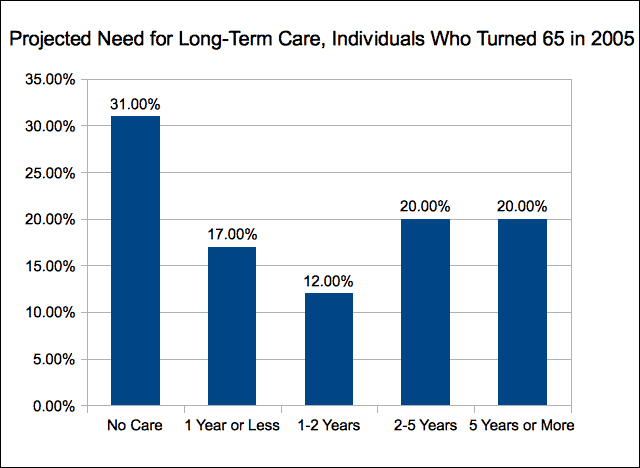

Most of us are familiar with healthcare – after all, we begin receiving healthcare at an early age. You may be unfamiliar, however, with long-term care, a form of care for individuals, usually seniors, who require ongoing care to perform activities of daily living such as bathing, using the bathroom, and cooking. The majority of Americans, around 70%, will require long-term care during their lifetimes. We expect that number to rise with life expectancy, as you are more likely to need care as you get older. In a study funded by Georgetown University, three researches calculated the probability of a 65 year old needing long-term care in the future. The chart below shows their findings, expressed as the percentage of 65 year olds who will need care for each length of time.

There’s a very good chance that a given senior will end up needing long-term care, and a 40% chance that he or she will require care for two years or more. Genworth Financial, an insurance company, releases a report each year about the costs of long-term care. Much like general healthcare, these costs are rising faster than the rate of inflation. Here’s a table comparing LTC costs in 2012 and 2013.

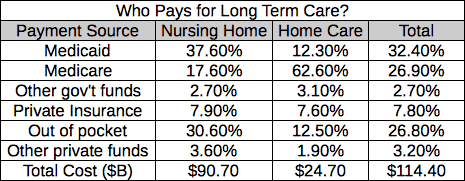

It is important to note that these costs were not factored into the health care expenditures that we mentioned previously. Seniors will in fact need to find even more resources to cover these costs. Most Americans believe that Medicare and Medicaid will cover the costs of long-term care. These programs do cover some of the costs, but according to this research from the Centers for Medicare & Medicaid Services, nearly 30% of nursing home & home care costs are paid for out of pocket.

A Retirement Security Crisis?

So far, we’ve established that the American population is growing older, that Americans are living longer, and that health care and long-term care costs are rising rapidly. Taken together, these forces may cause serious problems to retirees over the coming decades.

Guides & Featured Content

- The Benefits of Working Later Into Life

- Financial Stress Coping Guides for Seniors

- Grey Divorce - Coping and Moving Forward

- Life After Losing Your Spouse

- Using Technology for Better Money Management

- The Truth About Early Retirement

- Aging & Demographic Trends in the United States

- Senior Housing Association Directory

- The Caregiver Guide